Two weeks back, Today published this article titled “Young homeowners who bought ageing flats: What’s the deal?”. In it, they spoke to some such young homeowners “to find out why they bought flats they might outlive and the concerns they might have.” Well Today never spoke to us, but the Husband and I are part of the group whose “resale flat will expire before they turn 95”. So here is our unsolicited two cents on the matter and why we think that our decision makes financial sense.

Property as an investment and appreciating asset

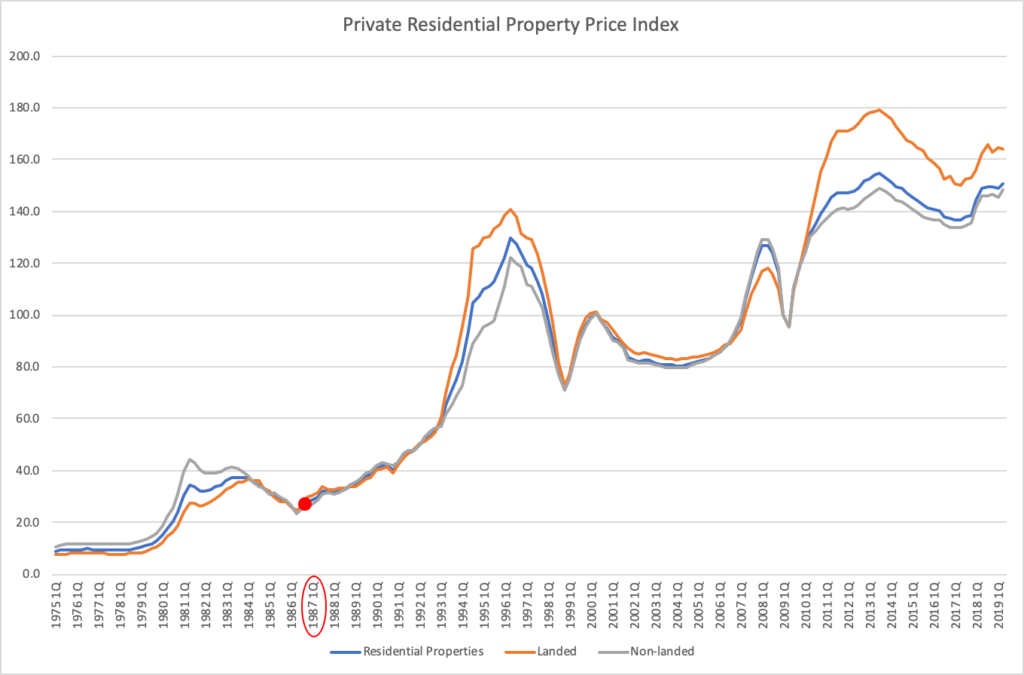

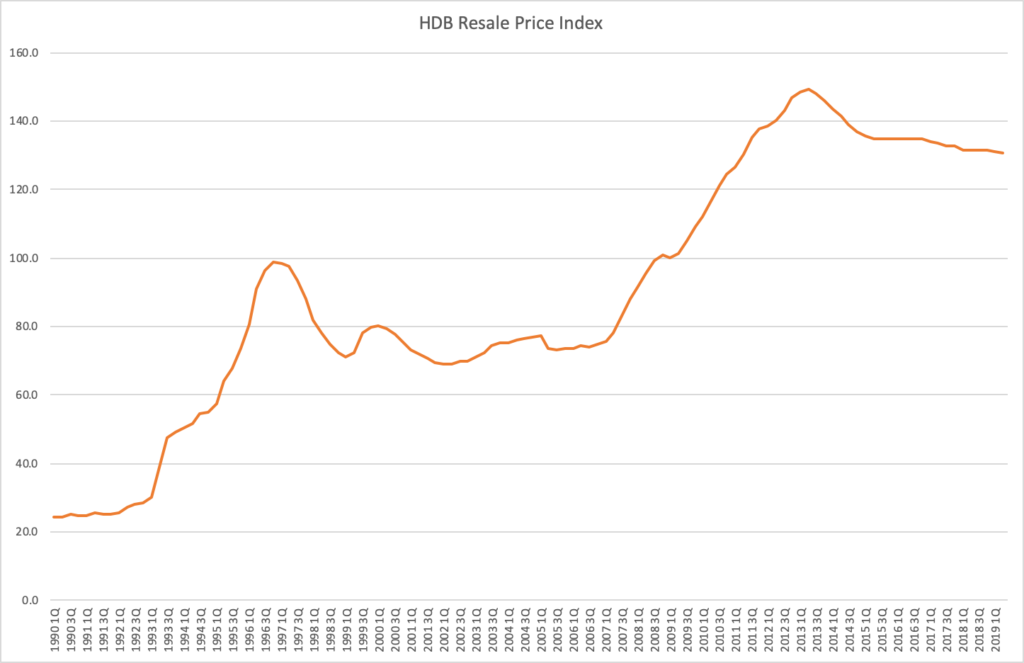

Growing up in Singapore, we often hear adults talk about property as an investment or an asset which is supposed to increase in value over time. I mean, that does make a whole lot of sense for if we look into the data. If we look at both the HDB Resale Price Index as well as the Private Residential Property Price Index from the time most of our parents (the “adults” in our minds) bought their homes in the 80s to early 90s, everybody basically made really good money on their houses whether they bought private or public housing. This is probably why Minister Wong found himself in a tricky situation after some 2017 blog post but more on that later.

Data from the URA via Singstat

Data from the HDB via Singstat

Our Home as a (Financial) Liability

Despite all that we were hearing growing up, the husband and I went into this home-buying business with no doubt in our minds that the house we were looking to buy was for us to live in, and therefore a liability and not an investment. I guess one could make the case that it still is an asset which might increase in value over time such as the people who say…

“But the price of your house could increase over the five, ten, thirty years that you own it for!”

Yes… only as long as we have no other place to move into if we sell the place… the gains remain where they belong… on paper.

… or the ones who have other ideas on how to monetize…

“You can rent out extra rooms!”

Yes… you technically could, only the rental from one or even two rooms is generally not quite enough to cover the mortgage. Also, it was our personal preference not to do so.

Deciding on how much liability we wanted to take on

This mindset that the home we live in is first and foremost a liability probably had the greatest impact on how we decided on what type of dwellings we would be looking out for.

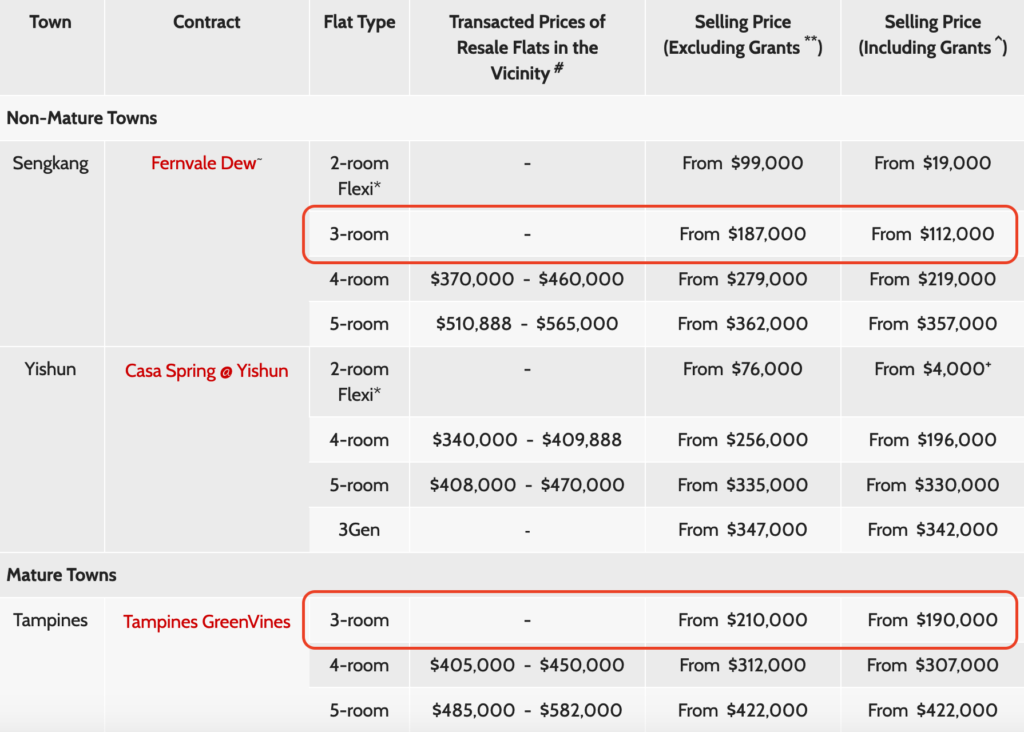

It helped us decide that we would definitely not be looking at private properties, and even amongst HDB flats, we would only be looking at 3 room flats. These tend to start in the ball park of S$180,000 both new (as seen below) and from the resale market.

Accessed on 12 Aug 2019.

Opportunity Cost of Waiting for New Flat

We ended up buying a resale 3 room flat for S$300,000 in a location which we found to work for our lives. We decided not to buy a new “Built-To-Order (BTO)” flat as we would likely end up having to wait 2-3 years for it to be built.

In addition to that wait, all buyers of HDB flats must fulfil a five year Minimum Occupation Period (MOP) from the day the purchase is completed. During this MOP, we cannot:

- Sell the flat in the open market

- Rent out the whole flat

- Invest in private property, both local and overseas

If we went the route of trying to purchase a new flat, it could be eight years before we could consider investing in another property. We found the opportunity cost of the three additional years a little much and hence went with a resale flat.

Renters or Owners?

We actually collected our keys the very week that Minister Wong gave what turned out to be controversial advice to young couples (such as us). These comments probably triggered a reaction because as mentioned earlier, we the people of Singapore are used to thinking of our homes as an appreciating asset. At some point, people started having discussions about whether people who “owned” HDB flats were renters or owners of their home.

The way we saw it, when we “purchased” our flat, what we were actually purchasing was this 69 year lease. There are a few advantages of being the owner of this lease as opposed to simply be renting this same house from whoever.

Rent-Controlled Apartment

First, the husband and I pretty much see our house as a rent-controlled apartment. I first encountered the up-side of rent-control when I met Liz (not her real name) on a camping trip in the Grand Teton National Park. Liz was a 60-something year old retiree living in San Francisco. She has been living in the same apartment for more than twenty years, and can only afford to continue doing so because of rent-control regulations.

For friends in Singapore who might not be familiar with these regulations: basically in certain US cities, rents can only be raised by certain amounts per year and the tenant can only be evicted for “just causes.” The means that even if the rental market improves drastically, landlords are technically not allowed to raise the rent drastically on their existing tenant. As such, the rent remains affordable for the tenant for as long as they continue living there.

And this is essentially how the Husband and I view the lease we have purchased. Making some assumptions about our mortgage, we will be spending approximately S$362,698 to have the apartment for the next 69 years. This works out to S$438 of “rent” per month if we were to divide that out by 828 months in 69 years. We find this to be a fair deal even if, as Minister Wong cautions, the lease runs to zero at the end.

Appreciation of the Asset

That said, I suppose commentators are also not wrong to say that HDB flat owners are owners. They are owners… of the lease. The lease, while it is running down, can too increase in value. Essentially the asset, that is the lease, can be an appreciating one.

If an MRT station gets built at our doorstep, people might be willing to pay significantly more for the remaining lease than what was paid seven years ago. If by then we have somewhere else to live, we could sell the lease off for a profit. If we were renters in the situation, we would likely end up with increased rent if an MRT station comes up instead of a lease that is worth more.

Image from LTA

Furthermore, as owners of the lease, we are allowed to benefit not only by selling off the least but renting out the apartment at more than our $438 per month if our circumstances allow it (again, another place to live in).

More money for the rest of life

In summary, the way we see it, we are okay to spend S$500 per month for the next 69 years on an apartment in Singapore. It frees up our money for us to invest in things which could bring other greater monetary and non-monetary gains.

What about you?